Stages of the process of making managerial decisions on an example. Examples of management decisions in the organization. Examples of programmed management decisions in an organization

Send your good work in the knowledge base is simple. Use the form below

Students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

Similar Documents

Basic concepts, classification groups and types management decisions. The essence of decisions and the order of their development. Evaluation of the effectiveness of managerial decision-making and methods of their analysis. Making a decision on the example of the company LLC "Your sausages".

term paper, added 06/19/2011

Concept, essence and characteristics management decisions. The main stages of development of management decisions. Factors influencing decision making. Practical use typology of managerial decisions on the example of the organization OOO "Medenta".

term paper, added 01/06/2015

Information support of the process of making managerial decisions. Implementation of decisions in the organization. Analysis and adoption of managerial decisions in conditions of certainty and uncertainty. Implementation of management decisions at the company OOO "Tsimus".

term paper, added 05/13/2010

Defining the goals and value system of the enterprise. Necessity, technique and methods of decision-making. Stages of development of management decisions. Development of a management decision by the method of collective generation of ideas. Basic principles of forecasting

term paper, added 02/22/2009

The essence and procedure of the decision-making process. Brief classification of management decisions. Inventory management models. Analysis and management decision-making under risk, conflict and uncertainty. Bounded rationality model.

term paper, added 10/03/2013

Features and classification of management decisions. Factors influencing management decision making. The main stages of the process of developing and making a management decision. Factor classification internal environment for specialized functions.

term paper, added 05/25/2014

The role of management decisions in the process of management, planning, organization, coordination and control. Decision making under uncertainty, the need to apply modeling in manufacturing organizations. Analysis of the decision-making process.

test, added 05/19/2010

Introduction

The relevance of the topic is determined by the fact that the life process of each organization is associated with the process of continuous change and development. An organization can achieve its goals only if its changes are adequate to the changes and requirements of the existing economic environment of market relations.

For state of the art science is characterized by a transition to a global consideration of the degree of development of the problem "Technology for making managerial decisions", many works are devoted to research issues. Basically, the material presented in the educational literature is of a general nature, and in numerous monographs on this topic, narrower issues of the problem "Technology for making managerial decisions" are considered. However, accounting is required modern conditions in the study of the problems of the designated topic.

The high significance and insufficient practical development of the problem "Technology for the adoption of SD on the example of a commercial enterprise" determine the undoubted novelty of this study. Further attention to the issue of "Technology for the adoption of SD" is necessary in order to use modern technologies decision-making is important for the leader, one of the main professional skills which is the ability to make effective management decisions. And in the fierce competition with other equal conditions successful, sustainable development and survival of those organizations that put themselves at the service of additional opportunities provided by technologies for making managerial decisions.

The topic of this work is the technology of making managerial decisions on the example of a trading enterprise CJSC "Vneshtorgsib - M"

The object of the study is the activity of wholesale - retail enterprise CJSC "Vneshtorgsib - M".

The subject of the research is the development of management decisions at the enterprise.

The purpose of the thesis is to study and evaluate experience, develop effective technologies in the process of preparing, making and implementing management decisions, as well as developing recommendations for their improvement.

To achieve this goal, it is necessary to solve the following tasks:

1. To reveal the theoretical foundations for the development of management decisions.

2. Identify problems in the development of management decisions.

3. Investigate the development of management decisions at CJSC Vneshtorgsib-M.

4. Suggest ways to improve the development of management decisions at CJSC Vneshtorgsib-M.

The following research methods are used in the thesis work: theoretical analysis of documentary and literary sources, analysis of documents, interview. The received research material was significantly supplemented by such a method as participant observation.

Knowledge. A significant contribution to the study of the problems of management efficiency, organization behavior in solving the set goals was made by economists and practitioners I. Ansoff, H. Wissema, P. Drucker, M. Porter, G. Simon, A. Strickland, S. Fisher and others. V.V. Glushchenko, A.G. Ivasenko, I.D. Ladanov, A.E. Saak, L.E. Sokolova and others. E.I. Brazhko, E.P. Golubkov, O.S. Vikhansky, I.L. Kardanskaya, L.I. Lukicheva, R.A. Fatkhudinov, E.Yu. Khrustalev, L.P. Yanovsky and others.

Of the foreign authors who worked on the problem under study: T. Boydell, N. Winner, F. Kotler, R.D. Lewis, M.H. Mescon, M. Albert, F. Hedouri, F. Harrison and others. Practical significance. The methodology and results of the study can be useful for organizing types of service industries. The developed recommendations make it possible to improve and improve the management decision-making system at the ZAO Vneshtorgsib-M enterprise.

The sources of information for writing a paper on the topic "Technology for making a managerial decision" were the basic accounting and reporting information on the enterprise CJSC "Vneshtorgsib - M" for 2004 - 2007.

The practical significance of the work lies in the fact that the developed recommendations make it possible to improve and improve the management decision-making system at the enterprise CJSC Vneshtorgsib-M.

Work structure. The study consists of an introduction, three chapters, a conclusion and a bibliographic list. The introduction substantiates the relevance of the choice of topic, sets the goal and objectives of the study, characterizes the research methods and sources of information.

Chapter one reveals general questions, reveals the historical aspects of the problem "Technology for making managerial decisions". The basic concepts are determined, the relevance of the sounding of the questions "Technology for making a managerial decision" is determined.

In chapter two, the content and modern problems of "Technology for making managerial decisions" are considered in more detail.

Chapter three is of a practical nature and, on the basis of individual data, an analysis of the current state is made, as well as an analysis of the prospects and trends in the development of "Technology for making managerial decisions".

Chapter 1. Theoretical basis development of management decisions

1.1 Essence and characteristic features of management decisions

There are many definitions and interpretations of the concept of "management decision". Here are some of them:

1. A management decision is the result of analysis, forecasting, optimization, economic justification and choosing an alternative from a variety of options to achieve a specific goal of the management system.

2. Management decisions are, first of all, the creative and volitional influence of the subject of management, based on knowledge of the objective laws of the functioning of the managed system and the analysis of management information about its state, aimed at achieving the goal.

3. A managerial decision is a choice that a leader must make in order to fulfill the responsibilities due to his position. The global goal of developing and adopting any management decision is to provide a feasible and most effective option for moving towards the goals set for the organization.

4. Management decision is a creative act of the subject of management, aimed at eliminating the problems that have arisen in the management object.

5. Management decision is a creative, mental act of the subject of management, which, based on the requirements, goals and emerging tasks and using data analysis and information about the object, determines the program for the subsequent activities of the team and individual workers.

6. A managerial decision is one of the necessary moments of volitional action, consisting in choosing the goal of the action and the methods for its implementation.

7. A managerial decision is the result of a specific managerial activity. Decision making is the basis of management. Each managerial function is associated with several general, vital decisions that need to be implemented.

8. Management decision is the result of analysis, forecasting, optimization, economic justification and selection of alternatives from a variety of options to achieve a specific goal of the management system.

9. A managerial decision is a deliberate conclusion, to take some action or, conversely, to refrain from them.

One of the basic concepts and components of the actions of entrepreneurship and management is the concept of "solution".

The decision is called the choice of alternatives of a certain course of action to achieve the goal.

An alternative is one option to achieve a goal that excludes another option.

Management decision is the basis of the management process. To manage means to decide. The term "management decision" is used in two main meanings - as a process and as a phenomenon:

Management decision as a process is the search, grouping and analysis of the required information; development, approval and implementation of management decisions;

· A management decision as a phenomenon is a plan of action, a resolution, an oral or written order, etc.

The essence of management decisions is associated with the social, economic, organizational, legal and technological interests of the organization (Figure 1.1).

Rice. 1.1 The essence of management decisions

The economic essence of management decisions is manifested in the fact that the development and implementation of any decision requires financial, material and other resources. Therefore, every management decision has its own cost. The implementation of an effective management decision should bring direct or indirect income to the company, and wrong decision leads to losses, and sometimes to the termination of the company.

The organizational essence of a management decision is that in order to develop and implement SD, a company must have the following capabilities, including:

Form a workable team;

Develop instructions and regulations governing the powers, rights, duties and responsibilities of employees;

Allocate the necessary resources, including financial and information;

Provide employees with the necessary equipment;

Establish a control system;

Constantly coordinate the process of development and implementation of SD.

The social essence of a managerial decision lies in the personnel management mechanism, which includes leverage on an employee in order to encourage him to vigorous activity a team. These levers include:

Needs; - interests;

motives of behavior; - installations;

Human values.

The legal essence of a management decision is the strict observance of regulatory legal acts, as well as the charter and other documents of the company itself. Violation of the law in the development of SD can lead to the cancellation of the decision, legal liability for its implementation.

The technological essence of a management decision is manifested in the possibility of providing personnel with the necessary technical, information tools and resources for the development and implementation of SD. When planning the development and implementation of SD, the manager must simultaneously form a technological basis for it.

Through the solution, the goal, types, scope of activities, rights and responsibilities are established, the actual state of phenomena, objects at a given time, etc. is fixed.

Accordingly, a management decision is reflected in the form of various kinds of documents, for each form of development of a management decision, its own set of implementation forms is used (Fig. 1.2).

Rice. 1.2 Joint use of forms for the development and implementation of management decisions

Describing the reasons for the need for decision-making, it seems possible to single out decisions:

1. logically determined by the technology of the process;

2. random, the need for which arises if the problem is generated by factors that may or may not appear when goals are achieved.

Management decisions are usually classified according to the following grounds (Fig. 1.3, 1.4).

1. Depending on the degree, managerial decisions causing the need for development and adoption are divided into programmed, non-programmed.

Highly structured, i.e. resulting from the implementation of a certain sequence of actions and steps;

Weakly structured (non-programmed), required in situations that are new to a certain extent, not internally structured or associated with unknown factors.

2. By reason (nature of acceptance):

Intuitive decisions - a choice made only on the basis of a feeling that it is correct;

Based on judgments, accepted on the basis of knowledge and experience. They are based on a forecast of future results. The method guarantees the prevention of gross errors.

The rational way of solving problems is called the best. It involves the formulation of all possible alternatives, the development of a system of the preferred option.

3. According to the degree of novelty:

Traditional decisions make up about 90% of decisions made in recurring situations. They are mainly used at the middle and lower levels of management.

Decisions made in new situations, to solve new problems, are called original. They require collection and analysis additional information and manifestation of innovative abilities of the leader.

4. According to the degree of certainty:

5. By nature:

Strategic decisions - decisions regarding a set of actions aimed at achieving the goals of the organization through its adaptation (adaptation) to changes in the external environment.

Current solutions - solutions that develop and refine promising solutions and accepted within a subsystem or phase of one of its cycles, such as the development cycle.

Operational decisions - decisions covering production processes for the manufacture and supply of elements of a lower level, bringing the planned task to specific performers in each division.

6. By functional orientation:

Planning - based on a special study to form a conclusion about the possible development and results of any management process;

Organizational - provide for the formation of a new or improvement of the existing structure of the company's management, as well as a set of administrative measures to organize the implementation of the task;

Activating - to increase the efficiency of the task, they form decisions to enhance the activities of the company's employees through stimulation and mobilization;

Coordinating - in the event of the appearance of unforeseen interfering influences, they are necessary to harmonize the company's activities;

Controlling decisions are aimed at ensuring the timely implementation of plans and planned development milestones;

Informing decisions are aimed at familiarizing the initiators and executors of the decision with the information they need, as well as with the intermediate and final results of the task.

7. For reasons:

Situational management decisions are caused by events that disrupt the planned course of events. Usually these are current, daily decisions of the head. A large number of them indicates an inefficient management process and the possibility of a crisis.

Management decisions on prescription are determined by the relevant regulations.

Program management decisions are long-term and universal in nature, determine the main directions of development, are the basis for more detailed decisions designed to ensure the achievement of program objectives at each stage of its implementation within a certain timeframe.

Initiative decisions are made by managers who occupy a fairly high, dominant position.

8. According to the degree of regulation:

Regulatory decisions must be implemented, and do not imply any initiative.

Orienting decisions determine the possible options for the activities of employees, when certain conditions occur.

9. According to the number of criteria:

Single-criteria decisions allow evaluating alternatives based on one criterion (indicator), the degree of importance of which may depend on objective conditions or be determined subjectively by the decision maker.

When evaluating multi-criteria decisions, a system of indicators is used. This creates the necessary difficulties, since it is necessary to select and evaluate their impact on the final result.

10. By organization:

The individual form of organization of managerial decision-making is characterized by the fact that the head alone (individually) makes a decision and bears personal responsibility for it.

At collective form all team members participate in the decision-making process (based on voting or consensus).

The collegial form of decision-making means that the work of preparing and making a decision is performed by a group of specialists authorized for this by a team of employees.

Decisions that have quantitative characteristics (approval of the budget, attraction of investments, setting tariffs for land lease services).

Decisions that do not have quantitative characteristics (the formation of a corporate culture, the solution of personnel issues, the management of public relations) are subjective, since they are determined by the personality of the subject who makes them.

12. Direction:

Decisions for influencing the external environment of the enterprise concern the immediate environment, partners, customers, creditors;

Decisions for influencing the internal environment of the enterprise are associated with a managed system (for example, a change in the staffing table, which will entail a reduction in employees or the development of a new management structure, as a result, a new position of a top manager will appear).

13. By scale:

General - affect the entire enterprise, its production and financial and economic activities. General management decisions determine fundamental changes in the enterprise, as well as the further development of production (computerization of production and management processes, the transition to production new products, reorganization of the enterprise, etc.);

Private - relate to any subsystems that affect current issues (for example, about discipline, about dismissal of an employee, about changing the work schedule of a department, etc.).

14. According to the degree of alternativeness:

Certainty - the choice of an alternative in conditions where the results of each of the options are known exactly;

Uncertainty - the choice of an alternative in the face of the impossibility of assessing the likelihood of potential outcomes;

Probabilistic certainty - the choice of an alternative in the face of ambiguity in the results of the options.

15. By the nature of development and implementation (by style):

Balanced decisions imply that the efforts of the decision maker to find and evaluate alternatives are distributed approximately equally. These solutions are effective for performers with high classification and high self-esteem;

Impulsive decision implies that the preparation of alternatives takes much longer than the assessment, and the decision is subjective and risky. For the effective implementation of impulsive decisions, a high personal and professional authority of the leader among subordinates and his high charisma are required;

Inert decisions mean that the process of finding different solutions is slow and uncertain. Such decisions are secondary, and the cost of justifying them far exceeds the effort spent on finding options. They weakly activate the staff to implement decisions. Inert solutions are effective in the current process of management activities, good support from managers at all levels, and also, if possible, to lobby their interests in the external environment.

Risky decisions are characterized by a higher intensity of work at the stage of searching for alternative options than at the stage of their evaluation. Such decisions are characteristic of gamblers - players. These solutions are effective in the general positive attitude of the leader and performers, when a possible failure does not significantly worsen the material and social condition of the team. Risky decisions usually use insurance or other methods to reduce possible damage; Cautious decisions are characterized by the thoroughness of the leader's collection of all options, a critical assessment of alternatives, and a large number of approvals. Such decisions are effective in resolving problems related to human life and the state of its environment. For example, decisions related to the activities of personnel at nuclear, thermal and power plants

The composition, structure, content and form of management decisions are determined by the specified criteria and the classification basis. So, for all their potential value, decisions will remain only good wishes if they are not translated into concrete actions. It is better not to start a business at all than to make unfavorable, and even unlawful decisions only on the grounds that they are well known, convenient, or suit someone.

The main means of managerial activity that determine the technology of its implementation are information support, organizational management techniques, conditions for managerial activity (organization of the workplace) and, of course, professional, business, socio-psychological and other personal qualities of the subject of activity.

1.2 Main elements of management decisions, basic requirements for them

The result of the manager's work is a managerial decision. The whole activity of the organization depends on what this decision will be, it also depends on whether the goal will be achieved or not. Therefore, the adoption of a decision by a manager always presents certain difficulties. This is due both to the responsibility that the manager takes on and to the uncertainty that is present when choosing one of the alternatives.

The main element of each managerial decision-making process is the problem, which is understood as the discrepancy between the actual state of the managed object (for example, in the provision of services) to the desired or given, i.e., the goal or result of the activity. The development of a plan of action to eliminate the problem is the essence of the decision-making process.

The simplest, "ideal" decision scheme in Figure 1.5 assumes that the process is a co-current movement from one stage to the next; after identifying the problem and establishing the conditions and factors that led to its occurrence, solutions are developed, from which the best is selected.

Rice. 1.5 Steps in the decision-making process

A more detailed structuring of the decision-making process is shown in Figure 1.6, where each of the stages (statement of the decision-making problem, decision-making, choice and implementation of the decision) highlights the procedures necessary to implement the targets of each stage.

Thus, the basis for setting the decision-making problem is the occurrence of a situation that causes the appearance of a problem. The description of the problem situation gives an idea of the factors that need to be carefully analyzed and considered when solving. First of all, it is required to establish whether they are internal or external in relation to this organization, since the possibilities of influencing these two groups of factors are different.

To internal environmental factors wholesale - retail companies, to the greatest extent, include: development goals and strategy, production and management structure, financial and labor resources, procurement and sourcing, marketing, inventory management. They form an enterprise as a system, the interconnection and interaction of elements of which ensures the achievement of its goals. Therefore, a change in one or more factors at the same time causes the need to take measures of managerial influence aimed at preserving the properties of the system as an integral entity.

The first group of external factors is practically uncontrollable by the managers of the organization, but it has an indirect (indirect) influence on its activities, which must be taken into account. It refers to the state of the macroeconomic environment in which a particular industry operates. Usually these are economic socio-demographic, political, legal and technological factors. For example, the economic state of a country (region) affects the work of an organization through such environmental parameters as the availability of capital and labor, price levels and inflation, labor productivity, buyers' income, government financial and tax policies, etc. Thus, inflation leads to a reduction in purchasing power. ability and reduces the demand for the products produced by the organization. An increase in the level of prices for products of related industries causes a corresponding increase in production costs in the organization, which results in an increase in prices for its products and can cause an "outflow" of a certain group of consumers. When their incomes are reduced, buyers change the composition and structure of consumption, which can also affect demand. The level of scientific and technological development in the country has a strong influence on the structure of the economy, on the processes of automation of production and management, on the technology by which products are manufactured, on the composition and structure of the personnel of organizations, and, most importantly, on the competitiveness of products and technologies. Accounting for numerous and diverse environmental factors, choosing the main ones among them and foreseeing possible changes in their mutual influence is the most difficult task facing leaders and managers.

The second group of external factors are less susceptible to influence by the managers of the organization. It includes the state of the microeconomic environment, which denotes aspects of the external environment that directly affect the organization due to its close interaction with the internal structures of the organization. In such a business environment, competitors, suppliers, consumers, labor markets and financial institutions operate, which initially shape the plans and activities of the company.

A necessary element (and parameter) of the managerial decision-making process is the assessment of the actions that are taken at its various stages.

A managerial decision is a decision made in trading system and directed: management of managed activities; marketing planning; financial planning; control by human resourses; interaction with the internal and external environment.

Thus, the decision-making process in retail trade should be carried out taking into account the characteristics of this area of the economy, as well as the influence of internal and external factors and constraints. This will help improve the quality and validity of decisions at all levels of management.

At the first stage, the target setting is most often used as a criterion for recognizing a problem, by the deviation from which the problem is judged.

The decision development stage begins with the collection and processing of the information necessary to develop a course of action.

At the stage of selecting and implementing a solution to a problem, various criteria are applied to select from a variety of project proposals acceptable ones, and from them - the most useful or preferable for solving the organization's goals. The quality of management decisions depends on how reasonably they are chosen, and this, in turn, determines the competitiveness of the organization, the speed of its adaptation to changes in the economic situation and, ultimately, efficiency and profitability.

Decision makers are called decision subjects. These may be individuals or groups of managers who have the authority to make decisions. In addition, experts can be involved in the process of development and decision-making at all its stages - specialists in specific problems, procedures, stages. Experts can provide significant assistance in setting the problem, in developing possible situations; they can set goals and set limits, develop solutions and evaluate their consequences, and so on. Experts are responsible for their recommendations.

Management decisions developed and adopted in organizations affect the interests of many people. The leader must be able to explain to the performers, top management, why he made this or that decision. There are a number of requirements for a managerial decision table 1.1.

Requirements for management decisions and conditions for achieving

| Requirements for SD and conditions for their preparation and implementation | Conditions for achieving requirements |

| 1. Compliance of SD with the current legislation and the company's statutory documents | 1.Self-control 2.control by a lawyer, referent |

| 2. Availability of official powers (rights and responsibilities) for the RDP | 1. Implementation of job descriptions 2. Availability of complete and reliable information about departments and services |

| 3. The presence in the text of SD of a clear target orientation and targeting (executors should be clear what the solution being developed is aimed at and what means will be used) | 1. Bringing to each performer his role in management decisions 2.Formulirovka for each purpose, timing, resources. |

| 4. Correspondence of the SD form with its content | Control by a lawyer, referent |

| 5. Achieving timeliness (no rush or late) | 1. Knowledge and intuition of the leader 2. Real assessment of the situation |

| 6. The absence in the text of the solution of contradictions to itself or previously implemented solutions | 1.Self-control 2. Control by a lawyer, referent |

| 7. Possibility of technical, economic and organizational feasibility of SD | 1. Conclusion of specialists who understand the problem 2. Conclusion of the company's experts |

| 8. Availability of parameters for external or internal control of SD implementation | 1. Operational control 2.Professional audit |

| 9. Accounting for possible negative consequences in the implementation of SD in the economic, social, environmental and other areas | 1.Conclusion of external experts, 2.Risk assessment |

10. Possibility of a reasonable positive result |

1. set (complex) of calculations for risky events 2. assessment of the true value of this management decision 3.Strategic forecasts for the development of the company in the implementation of this decision |

So, the presented scheme of the decision-making process reflects the logic of management activity, and not its complexity. In practice, this process is more complex and allows not only the sequence, but also the parallelism of a number of procedures, which can significantly reduce the decision-making time. It helps to identify important problems of a particular company, as well as the degree of uncertainty in which it operates. The effectiveness of this process largely depends on the methods that managers and leaders operate in performing all the necessary types of managerial work.

1.3 Algorithm and methods for making managerial decisions

The most important organizational aspect of the development and implementation of management decisions is the organization of the sequence of work required to complete this process. Here, the type of management that exists in the enterprise is of particular importance.

The theory of algorithms defines the concept of "algorithm" as a precise prescription that determines the process of information transformation. Decision development algorithm - a logical sequence of operations for the development of a management decision

Consider possible algorithms for the development and decision-making process for various types of management.

1. Under traditional management:

Identification of the problem;

Collection of information;

Information analysis;

Identification of the problem from the previous one;

Forecasting by analogy;

Evaluation and verification of solutions;

Adoption, registration, bringing to the executors of the decision, its execution, control of implementation.

Thus, decision-making in traditional management is based on studying past experience in solving similar problems, as well as predicting consequences by analogy with previously observed consequences. These features leave their mark on the decision-making algorithm, which includes stages related to the identification of a similar problem and the prediction of results by analogy with those already obtained.

2. With system management:

Identification of the problem;

Collection of information;

Analysis of information about the system as a whole and about the relationships of its elements;

Problem diagnosis;

Determining the goals of element management when solving a problem at the system level;

Development of criteria for evaluating the effectiveness of the solution;

Development of options for possible actions on the subsystem that is the source of the problem;

Predicting these actions for the system as a whole;

Evaluation and verification of these actions;

Acceptance, registration, bringing to the performers, execution, control of execution.

Thus, in system management, when understanding the organization as a set of interrelated elements, decision making is based on the analysis of information about the system and its components, as well as predicting the consequences for the elements of the system and the system as a whole.

3. With situational management:

Identification of the problem;

Gathering information about the situation;

Analysis of information about the situation;

Diagnosis of the problem and situation;

Determining the goals of managing the situation in solving the problem;

A list of possible actions to resolve the situation, forecasts of their consequences;

Verification, evaluation of solutions;

Adoption, execution, bringing to the executors, execution, control over the implementation of decisions.

The situational approach focuses on the fact that the suitability of various management methods is determined by the situation, therefore, the decision-making algorithm includes the stages of collecting and analyzing information about the situation, determining the goals of managing the situation when solving a problem, and predicting the consequences of control actions for the situation.

4. With social - ethical management:

Collection and analysis of information about the managed object (about problems and how it was solved);

Problem definition;

Determining the goals of solving the problem;

Development of criteria for evaluating an effective solution;

Prediction of consequences for various solutions;

Development of criteria for the optimal solution;

Verification of options;

Choosing the optimal solution;

Design, bringing to the performers, execution, control.

In social and ethical management, special attention in decision-making is paid to taking into account the permissible and not permissible consequences of options for control actions for various parameters.

5. With stabilization management:

Identification of the problem;

Collection of information about changing parameters;

Information analysis;

Problem diagnosis;

Determination of management objectives when solving a problem;

Development of decision evaluation criteria;

Study of the dynamics of the parameters of the control object;

Determining the time during which the object can still be stably controlled;

Distribution of available time for the preparation and execution of decisions to stabilize the managed object;

Development of solutions;

Forecast of the consequences of their application;

Evaluation of the implementation of various options;

Choosing the best option;

Acceptance, registration, bringing to the performers, execution, control.

Naturally, to solve specific problems using one or another type of management, these algorithms can be changed in accordance with the specifics of a particular problem.

In the process of developing and making managerial decisions, the decision maker can apply various methods that directly or indirectly contribute to the adoption of optimal decisions according to various criteria.

In the literature on management and decision-making technology, there are various approaches to the classification of methods. In this paper, a classification is adopted according to the degree of formalization: non-formalized, formalized and combined. The criterion for referring to a particular group is the use of quantitative methods of information.

Non-formalized (heuristic methods) of decision making are distinguished by a creative approach to finding alternatives; they are based on the analytical abilities of the decision maker.

The advantage of informal methods is that they are applied quickly. The disadvantage is that the methods do not always guarantee the choice of error-free solutions; intuition can also fail the manager.

Figure 1.8 shows the characteristics of a sample of non-formalized methods for developing management decisions.

Rice. 1.8. Non-formalized methods of making managerial decisions

Gordon method. The essence of the method: the formation of a working group of non-specialists on the problem under consideration. Purpose and conditions of application of the method: to overcome the established ideas in solving the problem under consideration. Features of the method: use non-traditional approaches in solving the problem.

Method of motivational research. Essence: the most important type of marketing research (mainly qualitative), which consists in studying the motives for buying a certain product / service at the unconscious, subconscious and conscious levels of the buyer's psyche. The purpose and conditions for applying the method: to improve the company's marketing policy in order to increase demand for goods / services.

Method of morphological analysis. Essence: possible combinations of solving the problem are identified and then studied. A morphological matrix can be used, where solutions are located by sinks, and elements of the problem itself are arranged by columns.

consumer expectation model. Essence: the model is a forecast based on the results of a survey of the organization's customers. They are asked to assess their own future needs as well as their new requirements. By collecting all the data obtained, the manager can accurately predict aggregate demand.

Method round table. Essence: in accordance with the method, a special commission, which is part of this round table, discusses relevant issues in order to harmonize opinions and develop a unanimous opinion.

inventory method. Essence: compiling a list of difficulties that stand in the way of solving this problem, discussing options for eliminating or overcoming barriers in making and implementing a decision.

The formalized methods for developing solutions are based on a scientific and practical approach that offers the choice of optimal solutions using EMMM and computers. This can also include statistical methods, they are based on the use of information about the past experience of the organization in any field of activity for development and implementation and are implemented by collecting, processing and analyzing statistical materials both obtained as a result of real activity and artificially developed by mathematical methods. computer simulation.

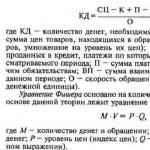

balance method. Essence: a method that allows you to make balance comparisons, linkages. For example, revenues and expenses, costs and profits are compared, and the most profitable option is selected.

Histogram method. Meaning: an illustration of the frequency of occurrence of individual parameter values appears in the form of a histogram. It shows (along the ordinate) for each parameter value (horizontally) the number of corresponding cases or their share in the total number of cases. The histogram shows the frequency of occurrence of average values. Can be chosen different variants solutions, but more often the most probable ones are chosen.

Game theory method. The essence of the method: assessment of the impact of the decision on competitors. Purpose and conditions for applying the method: it is used to determine the most important factors that need to be taken into account in a decision-making situation in a competitive environment. Features of the method: it is not used so often due to the complexity and dynamism of the external environment.

Factor analysis method. Essence: the analysis allows for the maximum possible consideration of the totality of variables that characterize the object and the relationship between them. At the same time, the forecaster is forced to seek a compromise between the number of variables in the description, which reflects the completeness of the forecast, and its complexity, labor intensity.

Functional cost analysis method. The essence of the method: identifying areas of imbalance between the functions of the object and the costs of them. Purpose and conditions of application of the method: used to select solutions and optimize the costs of performing the functions of an object without compromising their quality. Features of the method: has a high practical usefulness.

IDEF modeling method. The essence of the method: analysis and development of systems. Purpose and conditions for applying the method: it is used for modeling and analyzing the activities of enterprises, as it provides a rich set of opportunities for reengineering business processes. Features of the method: the method is based on the technology of structured analysis and development.

Combined methods for developing management decisions combine elements of non-formalized and formalized methods, shown in Figure 1.11.

SWOT analysis method. Essence: SWOT methodology analysis involves establishing strong and weaknesses the internal environment of the organization, as well as identifying opportunities and threats to its external environment. Establishing chains of links between these parameters allows you to develop strategic directions (goals) for the development of the organization.

Delphi method. Essence: analysis of the situation by generating ideas, discussing them, evaluating and developing a collective point of view. Purpose and conditions for the application of methods: used to discuss the problem that has arisen and to establish the main factors that determine its further development. Features of the method: high requirements for the level of qualification and competence of the leader who leads the meeting of experts.

Decision tree method. Essence: This is a schematic representation of a decision problem. Like the payoff matrix, the decision tree gives the manager the opportunity to “take into account different courses of action, relate financial results to them, adjust them according to the probability assigned to them, and then compare alternatives.” The concept of expected value is an integral part of the decision tree method.

Brainstorming method. Essence: This method is the most well-known of all group methods of using creativity. Brainstorming is applicable to a very wide range of problems. However, it is especially useful in diagnosing situations and suggesting alternatives. The main stages of applying the method of "brainstorming":

1. A small group is formed for work, preferably no more than eight people; 2. A chairman is selected to coordinate the activities of the group. The task of the secretary is to ensure that all ideas put forward are registered; 3. All members of the group become familiar with the situation; 4. The leader of the group gives a brief comment and communicates the purpose of the work; 5. As a result of individual work, group members put forward the maximum number of ideas in a limited time (usually half an hour); 6. All ideas must be registered; 7. Encouraged to use (not copy) the ideas of other members of the group; 8. Discussion or criticism of the ideas put forward is not allowed. This rule is especially important in brainstorming situations where it is very easy to show disapproval verbally or non-verbal means; 9. After the completion of the stage of putting forward alternatives, they are discussed and evaluated. At the same time, it is possible to put forward new ideas, which can be combinations, generalizations of previously put forward ideas, or completely new ideas.

The method is nominally group. Essence It differs from other group methods in that the stage of evaluation of individually put forward ideas is regulated in more detail. The nominal group method includes the following main stages.

1. Members create independent lists of ideas; 2. Each member of the group describes one of his ideas to the whole group; 3. Once all ideas are listed, they are discussed and evaluated by the group; 4. To reach a final decision, the members of the group vote separately for each of the ideas put forward.

Method of multi-stage survey. Essence: when using the multi-stage survey method, each expert should give an assessment on a predetermined scale in the interval, or arrange the objects by decreasing their value - ordinal ordering of any set of elements. To obtain a high-quality forecast, the participants of the examination are subject to a number of requirements:

High level of general erudition;

Deep specialized knowledge;

The presence of scientific interest in the object under study in the absence of material interest in this area;

Research experience in this area.

An important element is the anonymity of experts. It helps to avoid "pressure of authority", the emergence of interpersonal conflicts based on differences in status or social coloring of opinions.

Forced connection method. Essence: This method is based on the connection of ideas, but the degree of freedom is limited by the objects in question, which are usually chosen arbitrarily. Often the participants in the discussion turn to areas that they have never considered before. Forced linking is especially useful in situations where new uses are being sought for existing products or services.

Payment matrix method. The essence of the method: evaluation and comparison of alternatives according to several criteria. Purpose and conditions for the application of the method: in the conditions of the need to take into account several parameters when evaluating alternatives. Features of the method: the validity of the choice of criteria for achieving strategic goals is important.

So, the values of the decision will remain only good wishes if they are not translated into concrete actions. Methods can be generic, suitable for any problem, and can be specific. Which method to apply depends on the real content of the problem, and not on the knowledge, desire and ability of the manager or employee. It is better not to start a business at all than to accept unprofitable, and even unlawful methods, only on the grounds that they are well known, convenient, or suit someone.

So, for successful problem solving:

Firstly, to notice and analyze the problem in a timely manner in order to find out what led to its occurrence, and in fact strive to solve it.

Secondly, do not waste time on unnecessary decisions that do not affect the efficiency of the company.

Thirdly, constantly evaluate the effectiveness of the decision-making process, and subsequently the implementation of the decision.

Fourth, do not make multiple decisions on the same issue.

Fifthly, to involve employees related to them in the decision-making process already at the earliest stages of work, taking into account the correspondence of their qualifications to the degree of complexity of the problem; educate them as needed and don't forget to reward them for their success.

Decision-making technology is a set of scientific methods, models and techniques for developing and making managerial decisions.

Chapter 2

2.1 Characteristics of the enterprise and the mechanism for making managerial decisions at the enterprise CJSC "VNESHTORGSIB - M"

CJSC Firm Vneshtorgsib-M has been operating on the Russian market since 1993. Since its foundation, the company has focused on the supply and trade of imported goods.

The firm "Vneshtorgsib - M" is official representative the German trade mark "PAPSTAR" is the only large-scale project of goods for a cozy interior, a festive table, a cocktail and buffet, picnics and holidays, an aromatic line in Russia.

The goals of the creation of the society are: meeting the needs of individuals and legal entities in products (works, services) produced by the Company; Receiving a profit.

The mission of CJSC "Vneshtorgsib - M" is to meet the demand of customers by providing them with quality and related products at affordable prices.

CJSC "Vneshtorgsib - M" currently has the following divisions:

1.Wholesale base

2. Administration, located on the street. Kotovskogo 5

3. Shop "Gifts" on the street. Ordzhonikidze 27

4. Shop "Gifts" on the street. Kotovskogo 5

5. Shopping mall"Podmoskovye" opened in July 2006, the format of the cash-and-carry shopping center.

6 Dedicated station for renting and renting "Hobby" brand trailers, Germany and "Hymer" caravans,

Germany, trailers-tents brand "Camp-Let", Denmark, as well as their repair. Works since June 2007.

Figure 2.12 shows the share of activities of CJSC Vneshtorgsib-M in the total volume.

Figure 2.12 The share of activities of CJSC Vneshtorgsib-M in the total

Positive advantages in terms of internal resources are the following features:

The company has a high level of professionalism, which is important, as well as the desire of consumers to have an unlimited choice in the goods and services presented to them.

A positive factor is the presence of a developed logistics infrastructure, which allows you to plan stocks, make deliveries just in time.

The enterprise has implemented a partially integrated automation of business processes, automation of business management operations in accounting departments and stores, which allows making operational management decisions and adequately responding to market changes, a unified document flow has been implemented that speeds up business operations.

The range of the enterprise under study is presented by the following product groups in table 2.2:

Table 2.2 The range of goods presented in the subdivisions of CJSC Vneshtorgsib - M

A lot of attention is paid to the assortment formation policy at the enterprise under study - a constant assessment of the completeness and stability of the assortment is carried out.

When forming the assortment, the financial director of CJSC Vneshtorgsib-M focuses on the demand of end consumers of products. CJSC "Vneshtorgsib - M" strives to fully satisfy the needs of customers.

In order to intensify and stimulate sales, ZAO Vneshtorgsib-M uses advertising and public relations. The advertising spend limit is currently capped at 3% of revenue generated.

The main goal that is recommended to be pursued by CJSC Vneshtorgsib-M when organizing its own work can be reduced to the following: to help ensure that the company's advertising policy meets the consumer needs of potential buyers.

The organizational structure is presented in more detail in Annex 1.

The function of the head office is to direct activities and control, the entire decision-making process is concentrated in the head office.

In accordance with the current functional structure of enterprise management, the following composition of the main functions and services that ensure their implementation is approved, see Appendix 2 in more detail:

· CEO

Involved specialists – lawyer, translator, technical staff, security service.

financial department - financial director, finance manager;

accounting - chief accountant, accountant, senior cashier;

personnel department - head of the personnel department - clerk;

trade department - commercial director; deputy commercial director; wholesale manager, retail manager

Stores – division directors, section heads, senior salesperson, sales consultants

· Wholesale depot – director, merchandiser, sales consultant, driver, mechanics.

So let's give brief description functional duties company employees and departments.

General Director - he is at the head of the company, without a power of attorney represents on behalf of the Company; represents the interests of the Company in all Russian and foreign institutions, enterprises and organizations; enters into transactions on behalf of the company, with the exception of those, the conclusion of which is within the competence of the general meeting of shareholders, the Board of Directors and the Management Board of the Company; enters into labor agreements (contracts) with employees of the Company, with the exception of members of the Board of the Company; issues powers of attorney; issues orders and instructions binding on all employees of the Company.

The financial director is the right hand of the commercial director, develops the marketing policy at the enterprise based on the analysis consumer properties products sold and predicts market demand and market conditions.

The commercial director - this person on the scale of this company performs a large number of functions that were very interesting to me, as the future manager of the organization. Since the entire burden of the direct process of managing the movement of goods, compiling primary documentation, work with personnel (managers), organization and holding of meetings and presentations. And also, drafting commercial offers, managing money spent on advertising campaigns, business correspondence, etc.

Table 2.3 Functional structure of ZAO Vneshtorgsib-M

| Job title | Functions |

| Translator | Helps in negotiating with foreign companies, makes a transfer to the goods. |

| Lawyer - consultant | Development of legal documents, legal assistance to structural divisions of the company (shops) in preparing responses to claims. |

| Financial department | Carries out the development financial policy at the enterprise based on the analysis of consumer properties of the products sold and predicts market demand and market conditions. The department organizes the development of a strategy for conducting promotional activities in the media with the help of outdoor, illuminated, electronic, postal advertising, advertising on transport. |

| Accounting | The department maintains the organization's records required for both internal management purposes and for presentation to external users. The accountant reports to the CEO on the basis of the annual report, and submits a report on financial results. The director makes decisions on the results of the enterprise, decides on the target distribution of profits, the amount of funds, reserves. |

| Human Resources Department | Manages the work of staffing the enterprise with workers and employees of the required professions, specialties and qualifications in accordance with the goals, strategy, and profile of the organization, changing external and internal conditions of its activities. Ensures the preparation of documents for pension insurance, as well as documents necessary for the appointment of pensions company employees and their families. |

| Information technology department | Competent and accurate writing of new codes and names of goods, processing of documents in a single database. Correspondence with foreign partners. |

| Sales Department | Carries out activities for the supply and sale of products in order to increase the profits of the enterprise; plans and analyzes sales, takes measures to increase turnover; develops and implements measures to compensate for the decline in sales for seasonal groups of goods. Draws up contractual relations, orders goods, monitors underdeliveries and re-grading of goods; timely notifies suppliers about regrading and non-delivery of goods, requests certificates; makes an analysis of seasonal, calendar and other factors affecting fluctuations in demand. |

| Wholesale base | Carries out activities for the supply of products to the retail departments of the organization. Works with large wholesalers, by bank transfer. |

| The shops | They carry out activities for the sale of goods at retail, and work with small wholesale buyers. |

So, on this enterprise there is a functional principle of construction and specialization of the management process according to the functional subsystems of the organization. The functions of the head office of Vneshtorgsib-M are to direct and control activities, the entire decision-making process is concentrated in the head office. In CJSC "Vneshtorgsib - M" the final result recedes into the background, due to the fact that each service does not work to obtain it, but to fulfill its "mechanical" duties.

To increase the competitiveness of the enterprise ZAO Vneshtorgsib-M, it is important to have clearly defined and set goals and objectives, since it is a well-set goal that will affect the efficiency of the enterprise. It is also necessary that each division of the enterprise set a specific goal for itself, which, together with others, will help achieve a common goal. To achieve the goals of the enterprise, each department performs the appropriate tasks, respectively, the tasks also play a significant role in the internal structure of the enterprise.

The existing technology of making and executing decisions does not allow to bring the tasks of the upper level (profit, sales, saving resources) to all the lower divisions.

2.2 The process of making managerial decisions at the enterprise CJSC "VNESHTORGSIB - M"

Management decision-making is based on certain documentation. All documents that circulate in the document management system, CJSC "Vneshtorgsib - M" are divided as follows and are presented in Appendix 3.

The decision-making process is reflected in all aspects of management. Management activities in terms of the formation and implementation of decisions at the enterprise CJSC "Vneshtorgsib - M" consists of the following stages:

1. Preparation of a management decision

2. Providing procedures for making and making a management decision

3. Implementation of a management decision

4.Planning management decision

5. Control over the implementation of the solution

Table 2.4 Distribution of powers at the stages of decision-making technology in CJSC Vneshtorgsib-M

As can be seen from the stages of the process, managerial decision-making is highly dependent on the personal factor, since in fact decisions in the company are made by only one person, the general director.

With the help of the management matrix, one can illustrate the level of distribution of powers in making managerial decisions in an enterprise.

"1" indicates the actual responsibility.

"2" - general guidance.

"3" - the need to consult.

"4" - "opportunity" to consult.

"5" - must be notified

Table. 2.5 Distribution of powers in decision-making

| Director | Inform. Department | Fin. Department | Accounting | Personnel department | Sales Department | Subdivisions | |

| Activity planning | 1 | 5 | 3 | 3 | 5 | 3 | 5 |

| Conducting performance analysis | 1 | 5 | 2 | 3 | 5 | 3 | 5 |

| financial planning | 2 | 5 | 1 | 4 | 5 | 5 | 5 |

| Accounting | 2 | 5 | 2 | 1 | 5 | 3 | 3 |

| Marketing planning | 1 | 5 | 2 | 2 | 5 | 2 | 5 |

| Supplying the company with goods | 2 | 5 | 3 | 5 | 5 | 5 | 4 |

| Documentation of trade and technological operations | 1 | 5 | 3 | 4 | 5 | 4 | 5 |

| Human resource management | 1 | 5 | 4 | 5 | 3 | 4 | 4 |

We will assess the level of decision-making using a 5-point system (see Table 2.6).

Table 2.6 Evaluation of the level of decision-making by the personnel of the enterprise

| Decision maker | Decision quality assessment | Explanations |

| Director | 3 | Too authoritarian decisions, rarely uses the opinions of other specialists |

| Chief Accountant | 3 | |

| CFO | 4 | |

| Commercial Director | 4 | Attempts to be creative are manifested, limited by the power of the director |

| Head of Human Resources (clerk) | 3 | Solutions are formulaic, based on the instructions of the CEO |

| Division directors | 3 | Solutions are template, does not consider other alternatives and possibilities |

| sales staff | 3 | They do not show independence, rely on the instructions of the general director, director of departments |

So, as can be seen from the process of making managerial decisions, decision makers partially show attempts at a creative approach, but basically the whole process is implemented on the implementation of a specific decision set by the general director. The decision-making management process in ZAO Vneshtorgsib-M is authoritarian. The adoption of managerial decisions strongly depends on the personal factor, since in fact decisions in the company CJSC "Vneshtorgsib - M" are made by only one person - the general director

There is no informing of the personnel about the current results of the enterprise's activity, employees are informed about the changes taking place after the fact.

2.3 Typical problems of the enterprise CJSC "VNESHTORGSIB - M"

The inefficiency of the existing decision-making mechanism at the enterprise ZAO Vneshtorgsib-M is evidenced by the fact that the enterprise has an outdated management system.

The retail industry plays a big role in our lives. Therefore, retailers are commercial organizations that sell goods and services to the consumer for personal and household consumption. Retailers provide goods and services only by the piece, their customers are end users who buy goods and services for personal use and not for resale to third parties.

Like a service industry retail must rely on its employees to represent stores to the consumer, creating important points of contact with them. Therefore, personnel costs should be one of the most important expense items in the industry. However, the retail industry has a poor reputation as a job creator. Retailers must provide services to people when they really need them, which increases the length of the working day and work week in the industry.

Accordingly, one of the problems of CJSC Vneshtorgsib-M is the lack of qualified sales personnel. The company constantly has a turnover of salespeople - consultants, so after the new year, four salespeople quit at once.

In the course of the work, an oral survey of employees of the organization under study was conducted. 26 out of 36 employees were interviewed.

Let's analyze the received information.

Size wages.

80% of respondents noted average satisfaction with the size of wages. It is necessary to increase material incentives for employees by raising wages or organizing a system of bonuses and bonuses to raise the indicator.

Prospects for professional and career growth.

The survey showed that more than half of the employees do not see growth prospects in this organization.

Management should take a greater interest in the growth and progress of employees. This can be expressed in the fact that the employee will be entrusted with more complex work, you can delegate more responsibility to the employee for the performance of certain work.

Relationship with immediate supervisor.

80% of the respondents answered that they were not satisfied with this indicator.

The importance and responsibility of the work performed.

Only 40% of the surveyed workers meet this indicator. This is due to the small number of staff. It is important to understand that the mistake of even one employee can affect the financial position of the company.

Relationships with co-workers.

60% of the respondents answered that they were quite satisfied with this indicator. In the future, the organization should implement measures aimed at maintaining good relationships between employees.

Opportunities for independence and initiative in work.

All respondents answered that they were not satisfied with this indicator. The General Director of CJSC "Vneshtorgsib - M" should be given more initiative in the duties performed by employees.

CJSC "Vneshtorgsib - M" still manages to compete to some extent with large firms and federal operators, due to the ability to set low prices, being an official representative, due to the high quality of goods and shops located in the city center. And keep your market niche.

Important for the formalization of expert information is the ability of an expert to compare and evaluate the possible values of the features of the object of analysis by assigning a certain number to each feature. Depending on the scale on which these preferences are set, expert assessments contain more or less information.

In the general case, it is assumed that the opinion of a group of experts is more reliable than the opinion of an individual, i.e. that two groups of equally competent experts are more likely to give similar answers to a set of questions than two individuals.

The experts were asked to assess the strengths and weaknesses of the enterprise. Experts at the first stage of the analysis assessed the weight of each of the listed parameters for the industry. The parameter weight characterizes its importance, priority, in the total set of indicators.

Table 2.7 Analysis of strengths and weaknesses of ZAO Vneshtorgsib-M

Components of the internal environment |

The effectiveness of the components of the environment | Importance | |||||||

| neutral | |||||||||

| Marketing: | |||||||||

| Reputation of the organization and products | – | – | + | – | – | + | – | – | |

| Market share | + | + | |||||||

| Goods quality | + | – | – | – | – | + | – | – | |

| Production costs | – | – | – | + | – | – | – | – | |

| Distribution costs | – | – | – | + | – | – | + | ||

| Promotion efficiency | – | – | + | – | – | + | – | – | |

| Sales performance | – | – | – | – | – | + | – | ||

| Finance: | – | ||||||||

| Financial stability | – | – | – | + | – | – | – | – | |

| Debt | – | – | + | – | – | + | – | ||

| Inventory level | – | – | + | – | – | + | – | ||

| share price | – | – | + | – | – | + | – | – | |

| Level of innovation | – | – | + | – | – | + | – | – | |

| Financial Accounting | – | – | – | + | – | + | – | – | |

| Organization and personnel: | – | – | – | – | – | – | – | ||

| Entrepreneurial Orientation | - | - | + | – | – | + | + | – | |

| Management organization level | – | – | + | – | – | - | + | – | |

| Leadership Qualification | – | – | + | – | – | + | – | – | |

| Personnel qualification | – | – | – | + | – | + | – | – | |

| Rational distribution of rights and responsibilities | – | – | – | + | + | – | + | - | |

| System of values: | |||||||||

| Presence of traditions, symbols, rituals | – | – | + | – | – | + | – | – | |

| Motivation system | – | – | – | + | – | + | – | – | |

| Psychological climate in the team | – | – | – | + | + | – | – | ||

The external environment is of exceptional importance for commercial enterprises. To present it, we will briefly characterize the main parameters of the external environment, which also affect the enterprise ZAO Vneshtorgsib - M (Table 2.8).

Table 2.8 The external environment of the enterprise CJSC Vneshtorgsib - M

| Macroenvironment |

The tax burden is large and does not allow business to develop actively High customs duties, registration and market licensing Inflation is on the rise The political situation in the country has stabilized There are many unemployed in society, including in the industry Constantly improving quality characteristics |

| Immediate environment |

Inability to maintain the matrix of goods imported from Europe due to the constant change in the assortment by manufacturers Buyers are price sensitive Income growth of the population and firms The time schedule for the delivery of goods is determined depending on the type of product and ranges from one to several months. Entry into the market of competitors with lower costs |

Using the matrix "importance of efficiency" in the table, according to the results of the analysis, we will compile the highest and lowest importance, which is worth paying attention to (Table 2.9)

Table 2.9 Importance-Effectiveness Matrix

| Importance | Efficiency | |

| low | high | |

| high | Requires special attention Production costs; Distribution costs; financial instability; Motivation system; Psychological climate in the team. |

Maintains a high level Product quality; Availability of exclusive products; Long-term contracts with key exporters |

| low | Low priority Reducing the crime situation in the country; Customs legislation remains unchanged; Lack of managerial training of a number of managers. |

Overemphasis on unimportant factors Entrepreneurial Orientation Changing needs and tastes of customers |

So, the level of decision-making at the enterprise is low, this is reflected in its financial condition. Need to improve financial results, increase the market share and efficiency of the management system as a whole. To do this, first of all, the enterprise needs to improve the system of development and decision-making.

Chapter 3

It is recommended to the enterprise "Vneshtorgsib-M": - to implement in management the decision-making algorithm for situational management, described in clause 1.3; - allocate responsibility for collecting and analyzing information about the situation; - involve employees of the company in decision-making, with the provision of greater powers to them; - decision-making to carry out with the help of various methods of management decision-making technology. We will illustrate the application of these measures by evaluating the increase in the efficiency of financial accounting.

3.1 Efficiency of management decisions in ZAO Vneshtorgsib-M

Evaluation of the effectiveness of a management decision is determined not only by its validity, but also by the degree of its implementation in accordance with the requirements of the decision maker.

Efficiency comes from the word "effect", meaning the impression made by someone on someone. This impression can have organizational, economic, psychological, legal, ethical, technological and social overtones. The effect can be observed or formed.

Management of the effectiveness of a management decision is implemented through a system of quantitative and qualitative indicators, norms and quality standards.

The efficiency of the trading enterprise is ensured by the successful implementation of services. The resources of the enterprise and the requirements of cost-effective work to a certain extent limit the maneuvering, both in the range of services and in the prices for them. But it is the focus on customer demand and its active formation that should determine the use of available resources.

The ratio of the result and costs characterizes the effectiveness of any activity or phenomenon. It can be positive or negative. Thus, we can talk about organizational, economic and other efficiency.

In our case, we will talk about the effectiveness of financial results.

Trading activities of CJSC "Vneshtorgsib-M" are divided into main and management and auxiliary. The main activity involves the sale of goods, works and services. Auxiliary, performs repairs and reconstruction, construction of buildings, structures; repair of official vehicles, supply of materials necessary for the operation of the enterprise, etc. The manager performs regulatory and supervisory functions.

Let's focus on the main trading activity and consider the dynamics of changes in trade turnover in the table over the past four years.

Table 3.10 Changes in the turnover of the company CJSC "Vneshtorgsib-M"

| Indicator, thousand rubles | 2004 | 2005 | 2006 | 2007 |

| 1 | 2 | 3 | 4 | 5 |

| Trade turnover | 111945 | 134577 | 162111 | 195395 |

| 1 quarter | 17962 | 47652 | 26979 | 25296 |

| special services station | - | - | - | 6659 |

| 2 quarter | 26744 | 59911 | 43189 | 47200 |

| special services station | - | - | - | 9100 |

| 3 quarter | 29784 | 13572 | 45374 | 41617 |

| special services station | - | - | - | 9600 |

| 4 quarter | 37456 | 44214 | 46570 | 45783 |

| special services station | - | - | - | 10140 |

| Costs including: | 109480 | 133494 | 162038 | 196143 |

| - cost of goods | 43423 | 51167 | 61400 | 74035 |

| - materials used in the repair | - | - | - | 12166 |

| - rent and utility bills | 6030 | 6210 | 6320 | 7125 |

| - administrative | 4250 | 7145 | 9560 | 8956 |

| - remuneration of employees | 29545 | 32457 | 34120 | 43652 |

| - taxes | 9548 | 9231 | 10250 | 12511 |

| - nutrition | 2103 | 2468 | 2576 | 2874 |

| - acquisition of fixed assets | 487 | 1644 | 3674 | 2548 |

| - communication, information services | 316 | 531 | 562 | 463 |

| - vehicle maintenance | 1023 | 1455 | 1987 | 2145 |

| - general trade | 855 | 1520 | 1987 | 2650 |

| - technological costs | 1020 | 1999 | 2630 | 2880 |

| - transportation of goods | 3567 | 3658 | 5012 | 4950 |

| - general business needs | 410 | 623 | 755 | 987 |

| - construction | 6903 | 13386 | 21205 | 18201 |

| Financial results | 2465 | 1083 | 73 | -748 |

Considering the dynamics of sales, we note that the main demand for goods and services offered to the consumer falls on the second, third and fourth quarters of the year. The seasonality of demand for products is very important. Comparing four years, we note that every year there is an increase in trade by about 20 percent. This is due to the opening of the Kotovsky store in 2005, the Moscow Region store in 2006, and a specialized station on Chasovaya in 2007. In 2004, the territory was purchased, where the construction of a specialized station began and continues to this day. In this regard, in the next three years, the costs of the enterprise increased to the maximum for: the maintenance of additionally attracted workers; acquisition building materials and TMC; fixed assets. From the table you can see a stable increase in costs: in 2005 compared to 2004 they increased by 21.9%; in 2006 compared to 2005 by 21.4%; in 2007 by 21%, and compared to 2004 - by 79.2%. The diagram and graph of changes in income and expenses are shown in Figure 3.15, respectively.

Fig.3.15. Diagram of changes in income and expenses

Fig.3.16. Schedule of changes in income and expenses

According to the diagram, it is convenient to study the change in income and expenses for four years. Studying the chart, you can immediately pay attention to the point of intersection of income and expense. At this point, the company is on the verge of profit or loss. In connection with the expansion of activities, there was a need to increase the staff, so from 2004 to 2007 the number of employees increased from 42 to 70 people, which led to an increase in the payroll compared to 2004 by 47.7 percent.

With the increase in turnover, the cost of transporting goods increased by 38.7%.

Significant funds were required for the construction of the station. The company's own funds, which remained from retained earnings, were not enough, in connection with this, credit resources were attracted, the interest on which increased the item "administrative expenses" by almost 100 percent.

Administrative expenses also increased due to: recruitment costs, security services, legal services (documentation).

Rent, utility bills, communications, information services, and general business needs have not changed significantly in four years.

Although the turnover also increased compared to 2004 - by 74.5%, it can be concluded that the management staff, headed by the general, financial director and chief accountant, did not track the growth of costs, did not take measures to minimize them. This led to a deplorable result: by the beginning of 2007, the profit was replaced by a loss (748 thousand rubles). Also, wage arrears increased by 12,132.

For further analysis and management of costs, it is advisable to classify them into variable and fixed.

Variables:

Cost of goods;

Transportation of goods;

Materials used in the repair;

Remuneration of employees;

international negotiations;

Technological costs.

Permanent:

Rent and utility payments;

Administrative;

Nutrition;

Acquisition of fixed assets;